As its losses widen

further in Europe, Fiat has outlined yet another

presentation that offers a look at its proposed strategy

to solve its growing problems on its home continent –

although, as with previous presentations, the

correlation between projections and eventual reality

remains very much up in the air.

With

sales falling and a persistent lack of investment in new

models, Fiat sees its ‘quandary’ as offering two

choices. The first is to “remain focused on non-premium

mass-market and rationalise capacity by closing one or

more plants”; alternatively, it foresees a potential

future leveraging the “historical premium brand

heritage” of Alfa Romeo and Maserati, allied to a

re-alignment and repositioning of the group’s product

portfolio.

Fiat claims to prefer the latter option and proposes to

coalesce around five strategies which it also lists in

today's presentation:

1. Focus Fiat brand on 500 and Panda as pillar vehicles

(brands within a brand) and derive all future products

there from.

2. Reduce/curtail Lancia exposure, preserving uniqueness

of Ypsilon and rely on Chrysler’s NAFTA development to

feed European brand, if economically viable.

3. Focus on Alfa Romeo and Maserati to access higher-end

of ‘bi-polar’ market.

4. Fully flesh out Jeep brand by developing appropriate

products for European and international markets.

5. Continue to develop and maintain leading position in

LCVs.

Fiat adds that its overriding objectives are twofold.

The first is to utilise its EMEA (Europe, Middle East,

Africa) production base to develop its ‘global brands’ –

which it categorises as Alfa Romeo, Maserati, Jeep and

the Fiat 500 'family' – and secondly, to shift a

significant portion of its product portfolio towards

higher margin opportunities.

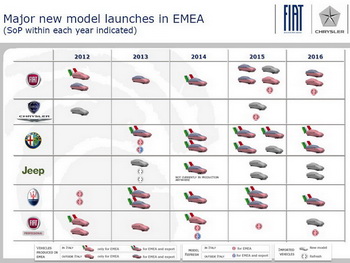

That is followed by another optimistic slide, which

lists 10 new Fiat models (including the 500L and Panda

4x4 for 2012, 500XL for 2013 and 500X for 2014), along

with a staggering nine from Alfa Romeo alone, by 2016,

with a refresh for the ageing MiTo and Giulietta

pencilled in for next year. The fundamental composition

of the Fiat brand is being reworked to centralise around

the 500 and derivatives, with the presentation

highlighting the company’s belief in its inability to

“leverage [the] Fiat brand to move into C-segment and

above.”

Worryingly for the group’s prospects as a volume

manufacturer, however, it was today reported in The

Wall Street Journal that, as a result of this

decision, the carmaker’s volume Punto and Bravo models

will be axed at the end of their life cycles, with no

replacements. The strategy appears to reflect

Marchionne’s belief that each individual product must

‘pay its way’, with no cross-subsidisation allowed for

models which cannot generate a profit – even if there

may be good reasons, such as the retention of market

share, to maintain a presence in certain segments. The

decision to scale back the Fiat brand to just A- and

B-segments, with the associated lack of presence in

significant volume segments, may help explain recent

media reports that Marchionne had proposed a merger

between three mass-market manufacturers in Fiat, Opel

and PSA. (Marchionne has since denied the reports.)

Moreover, a closer reading of Fiat’s plans is enough to

bring about scepticism as to their accuracy. For

instance, Maserati’s entire model range, including its

forthcoming Jeep-based Levant SUV, is now set to be

built in Italy – flying in the face of previous

assurances that the latter would be built at the

Jefferson North Assembly Plant in Michigan. Similarly,

Lancia’s sole scheduled refresh, due for the Ypsilon in

2015, is classified as an update which will come from an

Italian factory – yet the Ypsilon is currently

manufactured in Poland. The implication is thus that the

Ypsilon’s production will be moved from Tychy to Naples,

where it would be built on the Panda line. Whether

these, and a number of other plans, have been included

to satisfy various stakeholder interests in Italy, only

time will tell.

However, it should be noted that in its lack of

specificity about future plans, this outlook differs

from previous Fiat presentations. According to

Marchionne, this was a conscious decision. “We’ve had a

lot of internal discussions about whether I should

provide a higher level of granularity in terms of

product offerings and product launches,” he told

investors. “Because of the phenomenal amount of

consternation that has been caused after we launched

Fabbrica Italia back in 2010, and the inability of the

system to react to our reaction to a degrading demand

function, and the fact that that project effectively had

to be shelved due to changing market conditions, we have

decided to follow what our competitors have done

historically which is to not provide a lot of details

and effectively execute under development plans as they

saw fit.” However, critics have speculated that the

decision not to detail specifics is as much about being

able to more easily facilitate the inevitable changes

and cancellations to the plan, without breaking explicit

commitments.

Importantly for Italian car fans, the plan also

effectively foreshadows the axing of the storied Lancia

brand. Notably, Fiat management were unable to bring

themselves to admit the flawed nature of the plan to

rebadge Chryslers as Lancias; instead, ignoring the

various difficulties pointed out by a myriad of critics,

it is described in the presentation as an arrangement

“hindered by market condition[s]” and Lancia’s “limited

brand appeal” outside of Italy. Fiat’s solution for this

dilemma is to double-down on its commitment to

Americanise Lancia’s offerings, with Marchionne making

clear that, Ypsilon apart, the brand’s future – if

indeed it has one – lies solely in rebadged Chryslers,

built in North America.

Fiat sees synergies with this new strategy: “Products

needed for competitive offering in Europe are

complementary to those produced in NAFTA and LATAM where

production capacity is or will soon be saturated as

Chrysler product offering continues to be renewed

through 2015,” it says in the presentation. It adds the

target is to to utilise up to 15 percent of capacity for

export, especially for the forthcoming Jeep smaller SUV,

Alfa Romeo and Maserati brands.

Given that the company’s Italian factories currently run

at around 50 percent of capacity, it remains unclear how

they will be utilised if the push towards investment in

Fiat’s global ‘premium’ brands is only set to boost

capacity usage by around 15 percent, as around 80

percent usage is typically considered the minimum

threshold for profitable output. This also does not

include the decline in capacity usage which would result

from the axing of mainstream models such as the Punto

and Bravo.

Breaking down its EMEA targets, Fiat confirmed that its

2012 confirmed trading loss will come in at €700

million. It projects the next year’s European market is

likely to be flat, that the EMEA loss is expected to

come in at a similar or slightly lower level, and that

“actions on product plan and commitment of capital to

Italian manufacturing sites are dependent on respect and

compliance with new labour agreements; will require

24-36 months for implementation and will allow

Fiat-Chrysler in EMEA to recover some market share in a

more rational market and to act as export base for sales

by other regions.” Given the above preconditions, Fiat

believes that break-even is achievable in 2015-16.

Marchionne has also scaled back his production target of

6 million cars by 2016 (including Chrysler Group) to

4.6-4.8 million.