| SECOND

QUARTER FINANCIAL RESULTS & STATEMENT

OVERVIEW

The

achievements for the quarter are:

- A

significant reduction in the Groups operating losses, thanks to the progress

made by Fiat Auto, as it begins to implement its restructuring program

despite a difficult market environment;

-

A bottom line close to breakeven thanks to the gain on the sale of Toro

Assicurazioni;

-

An improved net financial position compared with the beginning of the quarter

due to a positive contribution of about 1.2 billion euros from the sale

of Toro Assicurazioni and lower than expected funding requirements.

The

quarter was also characterized by:

- The

presentation to the financial markets at the end of June of the Groups

Industrial and Financial Relaunch Plan. The Plan calls for the Groups

operating income to rise to more than 4% of revenues by 2006 as a result

of cost savings of 3.1 billion euros and higher margins on new products

for 1.6 billion euros, net of additional costs of 1.8 billion euros.

-

An acceleration of the pace of divestitures, with the closing of the sale

of Toro Assicurazioni to the DeAgostini Group (proceeds of about 2.4 billion

euros and gross gain of about 390 million euros) and the final signing

on July 1 of an agreement to sell FiatAvio (proceeds of about 1.5 billion

euros).

The

programs implemented during the quarter were followed by additional developments

in July, including:

- A

1.8-billion-euro Fiat SpA capital increase to support the implementation

of the Relaunch Plan.

-

The issue of about US$750 million in eight-year CNH senior notes. With

this transaction, more than 60% of CNHs indebtedness will be due in five

or more years.

Overall,

the transactions completed in the first half of 2003 and those slated for

closing later in the year will provide the Group with over 9 billion euros

in fresh liquidity, which it can use for its relaunch and development programs

and to repay maturing indebtedness.

RESULTS

FOR THE QUARTER

The

financial results achieved by the Fiat Group in the second quarter of 2003,

while indicative of a situation that remains challenging, are better than

those for the same period last year and for the first quarter of 2003.

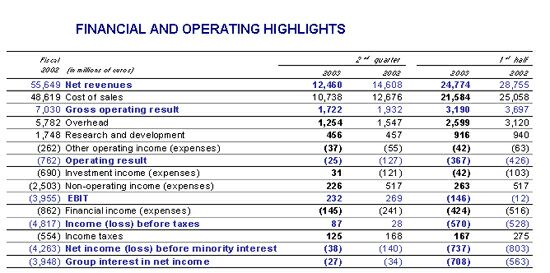

Consolidated

Group revenues totaled 12,460 million euros, down from 14,608 million euros

in the second quarter of 2002, when the figure included the contribution

of divested operations. On a comparable consolidation basis, the decrease

amounts to about 6%, mainly on account of changes in exchange rates.

The

Groups operating loss narrowed to 25 million euros, compared with operating

losses of 127 million euros in the second quarter of 2002 and 342 million

euros in the first three months of 2003. The quarter-on-quarter improvement

increases to about 150 million euros when the data are restated on a comparable

consolidation basis. The reduction in operating loss is due almost entirely

to the improved results that Fiat Auto was able to achieve despite difficult

market conditions.

The

consolidated net loss amounted to 38 million euros (loss of 27 million

euros after minority interests), compared with net losses of 140 million

euros (loss of 34 million euros after minority interests) in the second

quarter of 2002 and 699 million euros (loss of 681 million euros after

minority interests) in the first quarter of 2003. In addition to the reduction

in operating losses, the decrease in consolidated net loss reflects higher

income from equity investments, a decrease in financial expenses (due mainly

to the reversal of the loss on the total return equity swap on the General

Motors shares) and the net gain of 279 million euros earned on the sale

of Toro Assicurazioni. However, the contribution provided by extraordinary

items was significantly lower in the second quarter of 2003 than in the

same period last year, when it included a 547-million-euro net gain earned

on the sale of a 34% interest in Ferrari.

At

June 30, 2003, the net financial position showed net indebtedness of about

4.8 billion euros, or about 360 million euros less than at March 31, 2003.

This improvement reflects the net contribution (about 1.2 billion euros)

from the sale of Toro Assicurazioni, offset in part by the effects of the

sale of 51% of Fidis Retail Italia (about -440 million euros), changes

in working capital and the net loss for the quarter.

Fiat

Auto

During

the second quarter of 2003, demand for automobiles continued to decrease

compared with the same period last year, falling by 2.8% for all of Western

Europe and a steeper 6.8% in Italy. Over the same period, the market contracted

by a further 14% in Brazil, but the turnaround in Poland is continuing,

with shipments up 15%.

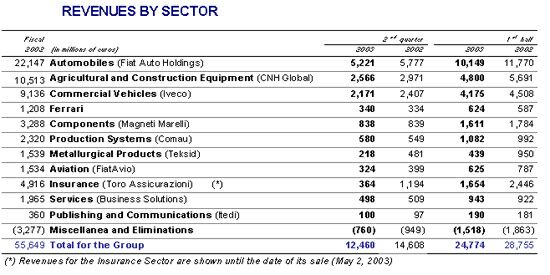

Fiat

Auto had revenues of 5,221 million euros in the three months ended June

30, 2003, compared with 5,777 million euros in the same period a year ago

(-9.6%, but -7.5% on a comparable consolidation basis). The Sector sold

448,000 vehicles worldwide. The decrease of 5.7% compared with the second

quarter of 2002 is due mainly to market weakness in Europe and Brazil and

to delays in buying decisions in anticipation of the introduction of new

models in key market segments for Fiat Auto (the new Fiat Punto, the Lancia

Ypsilon and, in the second half of the year, the new Fiat Panda and Idea).

Compared with 2002, Fiat Autos share of the automobile market declined

from 30% to 28% in Italy and from 7.7% to 7% in Europe. Sales of light

commercial vehicles remained strong, despite a rapidly contracting market,

especially in Italy.

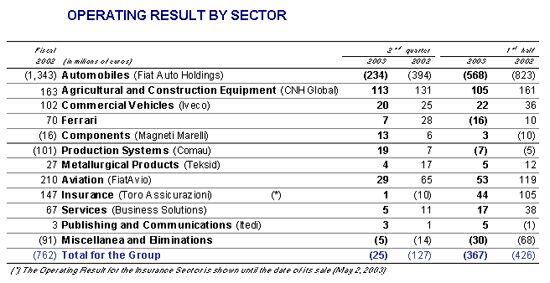

Fiat

Auto incurred an operating loss of 234 million euros in the second quarter

of 2003, down from losses of 394 million euros in the same period last

year and 334 million euros in the first three months of 2003. While still

negative, this performance is indicative of the significant progress made

thanks to incisive restructuring and cost-cutting measures and the growing

synergies developed through the industrial alliance with General Motors.

The resulting improvements were able to offset the negative impact of lower

sales and sales incentive programs offered to counter the effect of an

increasingly aggressive competition.

CNH

Global

The

market for agricultural equipment contracted in Europe (-3.9%), recovered

in Latin America (+11.6%) and benefited from an accelerating growth rate

(+22.1%) in North America, particularly in the segment of low-horsepower

tractors. Demand for construction equipment remained under pressure in

Europe (-3.4%) and Latin America (-20.2%), but turned around in North America

(+7.9%).

CNH,

which uses the U.S. dollar as its reporting currency, had revenues of $2,906

million, up from $2,719 million in the second quarter of 2002. Translated

into euros, revenues for the quarter declined to 2,566 million euros, down

from 2,971 million euros in the same period last year, due to the negative

impact of an unfavorable exchange rate.

Unit

sales of agricultural equipment were about the same as in the second quarter

of 2002 in all of the major geographic regions, but overall shipments of

construction equipment were down due to lower demand in Europe and South

America and increased competition in North America.

CNH

reported operating income of $125 million, compared with $118 million in

the same quarter of 2002. When stated in euros, operating income declines

to 113 million euros, down from 131 million euros for the three months

ended June 30, 2002. Better margins on new products launched this year,

higher prices charged for agricultural equipment and the positive impact

of profitability-enhancing programs contributed to the improvement in the

Sectors operating performance. However, in the comparison with 2002, these

positive factors were offset not only by an unfavorable exchange rate,

but also by a change in the sales mix, the reduction of production volumes

to cut company and dealer inventories, and higher medical benefit and pension

plan funding costs, primarily in the United States.

Iveco

The

weakness experienced by the European market for commercial vehicles (-3.8%)

was caused almost entirely by the sudden drop in demand that occurred in

Italy (-24.4%) once the investment tax credits provided by the government

through the Tremonti Law expired. An analysis by market segment shows a

sharp contraction in medium trucks (-10.6%) and less pronounced declines

in light (-3.5%) and heavy vehicles (-2.2%).

Iveco

had revenues of 2,171 million euros in the second quarter of 2003, compared

with 2,407 million euros in the same period a year ago. In addition to

unfavorable market conditions, which primarily affected sales of light

and medium vehicles, the decrease in revenues chiefly reflects the deconsolidation

of Fraikin (sold at the beginning of the year) and the Naveco joint venture

in China. On a comparable consolidation basis, revenues show a decline

of 3.5%. New models introduced late in the second quarter to broaden and

round out the Sectors product line (New Eurocargo in the intermediate

segment and Stralis Active Time and Active Day in the heavy-load segment)

are expected to develop their full sales potential in the coming months.

Iveco

reported operating income of 20 million euros, down from 25 million euros

in the second quarter of 2002. On a comparable consolidation basis, operating

income is about the same as in the second quarter of 2002.

Ferrari

Ferrari

posted slightly higher revenues (+1.8%), but operating income fell to 7

million euros (28 million euros in the second quarter of 2002). The main

reason for this decline is a substantial increase in research and product

development outlays, incurred mainly to relaunch the Maserati brand.

Other

Sectors

The

Sectors that produce components and production systems were affected to

different degrees by the difficult conditions facing carmakers and by the

negative impact of an unfavorable dollar-euro exchange rate.

Unfavorable

exchange rates and the divestiture of the Aluminum Division in September

2002 had a particularly strong impact on Teksid revenues and operating

income, which decreased to 4 million euros. Magneti Marellis revenues

were about the same as in the second quarter of 2002, but operating income

improved to 13 million euros thanks to production efficiency gains. Comau

posted an increase in revenues, especially in North America thanks to a

healthy order portfolio, and was able to return to profitability with operating

income totaling 19 million euros.

The

revenues booked by Business Solutions in the second quarter of 2003 were

basically unchanged from the comparable period a year ago, but operating

income decreased to 5 million euros due to the combined impact of the sale

of IPI and increased price competition, offset in part by efficiency gains.

Itedi reported operating income of 3 million euros.

RESULTS

FOR THE FIRST SIX MONTHS OF THE YEAR

The

overall results for the first half of 2003 are reviewed below.

- Consolidated

Group revenues totaled 24,774 million euros, compared with 28,755 million

euros in the first six months of 2002. On a comparable consolidation basis,

the revenue decline amounts to about 8% and is largely attributable to

changes in exchange rates.

-

The operating loss totaled 367 million euros, most of which attributable

to the first quarter (-342 million euros), down from the 426 million euro

loss in the first half of 2002. On a comparable consolidation basis, operating

result improves by about 110 million euros.

-

The consolidated net loss amounted to 737 million euros (708 million euros

after minority interests), most of which incurred in the first quarter,

as compared with a net loss of 803 million euros (563 million euros after

minority interests) in the first six months of 2002.

-

At June 30, 2003, the net financial position showed net indebtedness of

4.8 billion euros (net indebtedness of 5.8 billion euros at June 30, 2002).

The increase compared with December 31, 2002 is due to the net loss for

the period, a rise in working capital requirements and a decrease in discounted

receivables (both of which occurred mainly during the first three months

of 2003), offset in part by divestitures.

OUTLOOK

FOR THE BALANCE OF THE YEAR

During

the balance of 2003, the Fiat Group will continue to face difficulties

and challenges due to uncertain market conditions and the resulting increase

in competitive pressures. In this environment, the results achieved thus

far point to a further improvement in the Groups key operating and financial

performance indicators.

The

pace at which ongoing restructuring and cost-cutting measures are being

implemented is in line with expectations. During the second half of 2003,

and especially in the fourth quarter, the Group will begin to benefit from

the fresh momentum developed thanks to the 2003-2006 Relaunch Plan and,

more specifically, from an acceleration in the launch of new products by

all Sectors, which will be vital in enhancing profitability.

Given

this scenario, it is reasonable to expect for 2003 a further decrease in

the operating loss, which should be significantly lower than in 2002, and

a healthier financial position than at the end of last year.

CAPITAL

INCREASE

After

having been informed of the preliminary results of the capital increase,

the Board of Directors noted with appreciation that at the end of the exercise

period of the option rights, over 98% of the capital increase has been

subscribed.

|